.svg)

.png)

%201.png)

Product Updates

Coris MCP: Your merchant risk data, wherever you work

Coris MCP connects ChatGPT and Claude to your merchant risk data, letting teams query portfolios, investigate merchants, and take action from one conversation.

Embedded payments are transforming SaaS revenue models, with companies like Shopify and Toast earning over 70% of revenue from financial products. This guide explores four key approaches—Referral, Branded Payments, PayFac-as-a-Service, and becoming a PayFac—helping SaaS teams choose the right path for scaling payments.

What do SaaS companies like Shopify and Toast have in common? Over 70% of their revenue comes from embedded financial products.

SaaS companies selling to SMBs are increasingly offering embedded financial products in order to become a one-stop shop for their customers. Within embedded finance, payments are often the first financial product these companies offer, and they represent a significant revenue opportunity. Embedded payments are expected to generate $21B in revenues in 2026, up from $12B in 2020 (Source).

Given the success of payment facilitators (PayFacs) like Stripe, several players have recently emerged to offer SaaS companies additional ways to embed payments. These new players and their business models may be confusing, so we decided to write this “cheatsheet” article explaining all of the options.

There’s no “right” way to embed payments into a SaaS platform, but this article outlines key factors teams should consider when deciding on the appropriate model for their business.

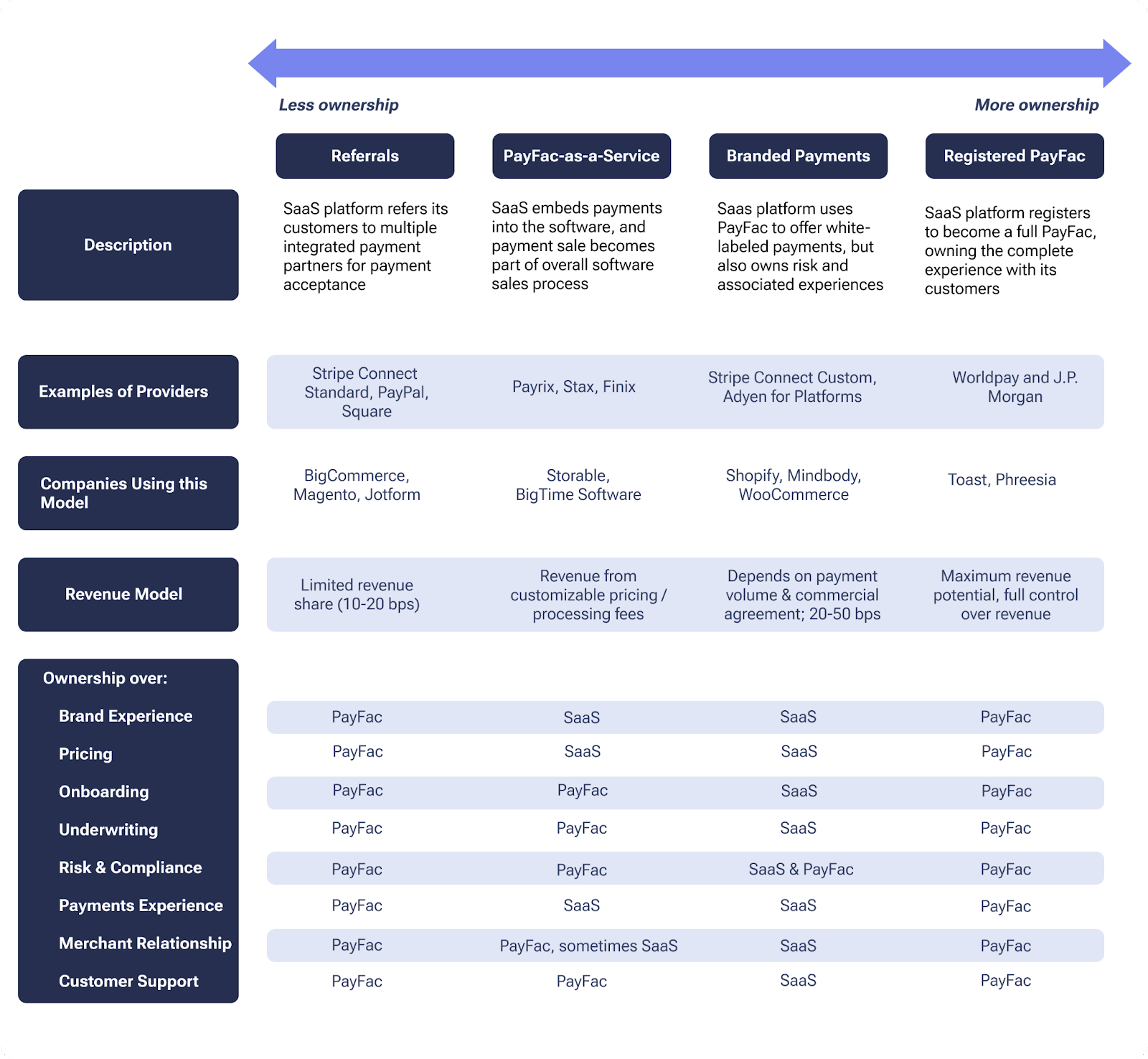

There are 4 main ways SaaS companies can implement embedded payments:

Under this model, a SaaS company “refers” its customers to one or multiple 3rd party payment providers to handle payments, and earns a limited revenue share from the transaction fees. This is a developer-friendly, low-cost way to offer payments to a platform, and allows SaaS companies to focus their resources on their core business. PayPal and Stripe Connect Standard are leading providers of referral payments.

Referrals are a quick way to add payments to a SaaS platform, but they come with limitations. First, SaaS teams lack control over the onboarding, underwriting and customer support process, which can negatively impact their customers’ experience. Additionally, referral payments can create a disjointed user experience. Lastly, since SaaS teams own less of the infrastructure/risk, they also earn a smaller share of the overall payments volume than they would in other embedded payments models.

PayFac-as-a-Service (PFaaS) is a newer model that allows SaaS teams to effectively “rent” payment facilitation capabilities from a company such as Finix or Payrix. At first glance, it sounds like the “goldilocks” approach to offering embedded payments:

While PFaaS does not offer full control over the customer experience, its hybrid approach can be a good fit for SaaS companies who are looking to graduate from referral payments, without investing significantly into their payment infrastructure. That being said, one common concern from SaaS companies heard in this model is the lack of control over the risk policies exercised by the PFaaS provider.

Under this model, SaaS companies partner with an existing PayFac to offer white-labeled payments on their own platform. Payments usually occur on the SaaS platform and are aligned with the company’s brand design. The SaaS platform controls customer support and takes on underwriting and risk management responsibilities, while the PayFac only controls compliance obligations such as onboarding/KYB and card network requirements. Stripe Connect Custom and Adyen for Platforms are leading providers of branded payments.

Branded payments offer SaaS companies the second highest degree of control over the customer experience and economics (after the PayFac model). It involves more effort than the previous two models, but SaaS companies don’t necessarily need to build out all of the infrastructure themselves. Certain parts of their program, such as risk management, can be managed by partners. For example, SaaS companies using Stripe Connect Custom partner with Coris to manage merchant risk management responsibilities, from onboarding to payouts.

Software platforms can become PayFacs themselves, meaning they help sub-merchants process transactions using their master merchant account. Of all the models considered, becoming a PayFac gives SaaS companies ultimate control over the customer experience and the greatest share of payments revenue.

Becoming a Payfac is most appropriate for large software companies that already have significant payments volume. Why? Becoming a PayFac is a time-consuming and resource-intensive endeavor: the registration process can take up to 2 years, and requires upfront investments in payments infrastructure and hiring for teams across product, engineering, operations, risk, and legal. Similar to the branded payments model, PayFacs can choose to leverage risk infrastructure partners to fortify their risk management capabilities. That being said, companies still need to have sufficient payments volume to justify these investments.

How you choose to offer embedded payments is a multifaceted decision, but hinges on one ultimate question: How important of a role will payments play in your company’s overall business and product strategy? If payments are central to the strategy - in other words, they happen frequently enough to impact trust with the platform - and you expect volumes to scale quickly, choose a payments model that gives you more ownership. This will allow you to tailor the payments experience to your customer base as much as possible.

Below we outline some more specific considerations to keep in mind when deciding on the right path for your team.

Product experience: How much control do you want over the user experience? Do you want the payments portal to be seamlessly integrated into your platform, aligned with your company’s brand design, or is referral to a 3rd party payment provider sufficient? Companies who want greater ownership over the user experience should opt for a white-labeled payment provider, as in the PFaaS and branded payments models. This seamless experience helps build trust with customers. Companies who require less UX control can opt for the referral model.

Brand experience: Referring to a 3rd party payment provider might be easier and quicker, but a referral model or having a “bring your own gateway” model might lead to other brands taking up valuable mindshare in your website/app. Brand dilution is something software companies don’t always think about until it becomes an issue, but wiser minds factor this in as part of their embedded payments strategy. Shopify is a great example of a company maintaining a strong brand presence, despite using a white-labeled payments provider.

Customer support: Can your customer base directly manage complex disputes and payment questions with a 3rd party, or do they need an intermediary? If you’re serving customers in more professionalized industries, they might have the knowledge or resources to directly manage disputes with 3rd party payment providers, as is the case under the referral and PFaaS models. However, if your customer base is primarily mom-and-pop shops, they may find these processes confusing and burdensome. The branded payments model and PayFac setup allow SaaS providers to be more hands-on in the customer support process. This can especially be helpful where use of your software can help them further, such as in the case of invoicing platforms.

Commercials: Will the company’s PayFac provide transparent pricing to your customers? Will they give you (the SaaS company) any influence or control on the pricing model? Payments are one part of a SaaS company’s offering, so it’s important to ensure the pricing model integrates well with your overall monetization strategy.

Data ownership: Who owns your customers’ KYC and payments data? PayFacs often own the contract with merchants (in this case, SMBs), meaning that you, as the SaaS provider, may or may not own your customers’ data. It’s important to get this clarity upfront, as it can impact your ability to provide comprehensive customer support, your ability to leverage merchants’ KYC data when building other embedded financial offerings, and your ability to port merchants to other providers and systems in the future.

Risk management: Last but not least, it’s important to consider the risk profile of your customer base. We suggest asking two sets of questions:

There’s no one-size-fits-all approach for offering embedded payments, and many companies shift between different models as their business needs evolve. Companies like Airbnb and Uber started out under the referral model and gradually built the embedded payments experience we see today. On the other hand, Thumbtack started out with an embedded payments experience and replaced it with a referral payments model as it scaled.

Your company’s payments strategy will evolve as the company scales. Choose a payments model that aligns with your current business and product strategy, and choose partners who can support you throughout the journey. Coris is proud to partner with SaaS companies utilizing any of the four payments models outlined.

Contact us if you’re interested in learning more about Coris’s risk management capabilities for embedded payments.

Follow us

.svg)